Angle Protocol: a Framework for Fixed Rate Lending

Introduction

Angle Protocol is considering investing some of its reserves (USDC, DAI) into Notional fixed rate lending to take advantage of the higher interest rates that Notional offers relative to money markets like Compound or Aave. To utilize Notional effectively, Angle should plan to hold its loans to maturity in order to avoid paying any costs associated with early exits.

This presents a challenge to Angle from a decision-making standpoint. Angle wants to maximize its returns, but as it increases its allocation to Notional it increases the risk that it will be forced to exit its fixed rate loan positions early and incur a cost for doing so. The analysis we do here will help guide Angle’s decision-making and assist in striking a balance between the benefit of lending on Notional and the risk of early exit costs.

We are proposing a simple, probability-weighted expectation framework to calculate how much money Angle should invest into Notional. To help guide this investment decision, we use historical Angle reserve data to calculate an estimate for the probability that Angle user redemptions would force Angle to exit its fixed rate loans early, and an estimate for that exit cost. Our analysis shows that Angle could easily lend up to 20M USDC with effectively zero risk of early redemption.

Based on our analysis, we believe Angle should lend $5M USDC over 6 months and $5M DAI over 6 months for an excess return respectively of 0.63% and 1.38% over the Compound rate. We find that the probability that Angle will need to exit loans of this size early is effectively zero. But even if Angle did need to exit early, we will show that in almost all cases, Angle would still be better off lending fixed on Notional rather than earning the Compound rate.

Assumptions

This model requires some assumptions. Our approach has been to prioritize simplicity and make conservative assumptions (i.e. the actual probability of early exit is likely lower than our estimates). Here are the assumptions we make.

- No underlying growth in the protocol. Angle is likely to grow its reserves over the following months as it develops integrations and improves its investment strategies, but we assume that its reserves do not grow beyond their current levels.

- No SLP stabilization mechanism. SLPs suffer from slippage when the collateral ratio drops below 120% and as a result they are unlikely to withdraw their reserves. Some of our simulations have the collateral ratio dropping to 105% and we have assumed no change in redemption probability under this circumstance.

- Incentives. We assume no incentives. Angle can increase incentives to attract SLPs into the protocol and stem outflows. As reserves decrease, the APR for SLP will increase as rewards are shared between less users. We ignore the potentially stabilizing effect of incentives.

- Full EUR/USD hedging. When users' reserves are fully hedged, Angle has to pay money to hedging agents when the USD strengthens against the EUR. As a result, USD reserves will decrease but stay identical in EUR terms. The reserves in USD terms are more stable when they are unhedged, but we assume this is not the case.

- Exclude liquid reserves and hedging agents collateral from reserves calculations. These are part of the working capital of the protocol. They are used to meet burns and repay the hedging agents when they close their positions.

- Assumed no insider money. In practice, the protocol will have insider or strategic investor money. This money is likely to remain in Angle putting a floor to the reserves.

It is worth noting that we have not modeled any security/hack risk which could lead to a drain on reserves.

Reserve Analysis Framework

Angle’s reserves are composed of 1) User Reserves 2) SLP reserves which provide the over collateralization. We base our modeling on historical data from the Graph, data starting in December 2021, to exclude the first month of operations. We look at DAI and USDC pools.

Once we have defined a probabilistic model for the deposits and redemptions, we run 5000 simulations, calculating daily reserves over a 3 and 6 month period. For each simulation, we then calculate the minimum reserves over the lending period.

We combine those simulations to calculate the probability that the reserves expressed in $ drop below a certain level (probability that we have to redeem our Notional lending). Daily redemptions or deposits for user reserves and SLP pools are modeled by the sum of a normal distribution (normal changes) and a Poisson distribution (for the impact of whale investors). We calculate these as a percentage of current reserves. We start from the initial reserves and add every day the simulated daily change to calculate the updated reserves. This simulates daily reserves positions for both user and SLP pools.

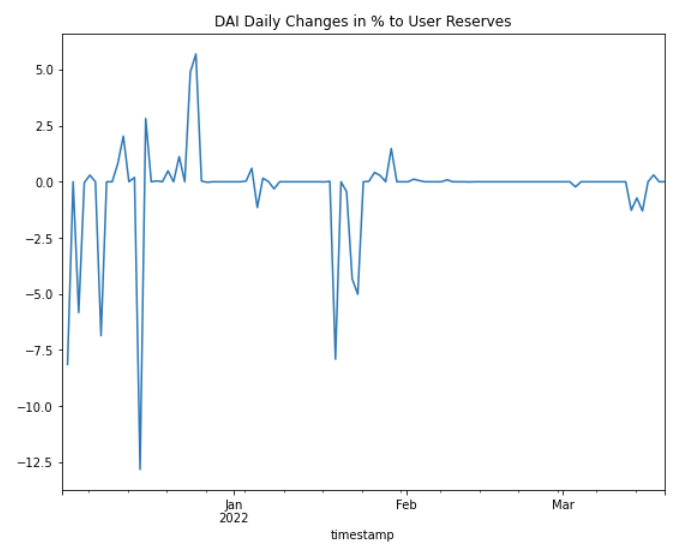

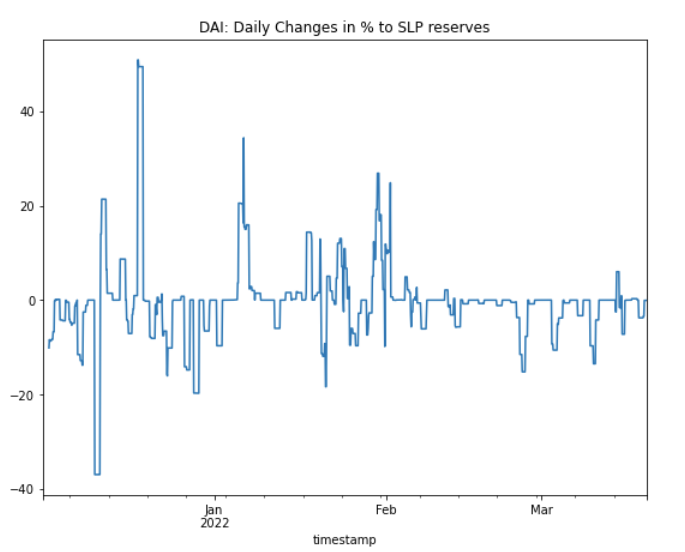

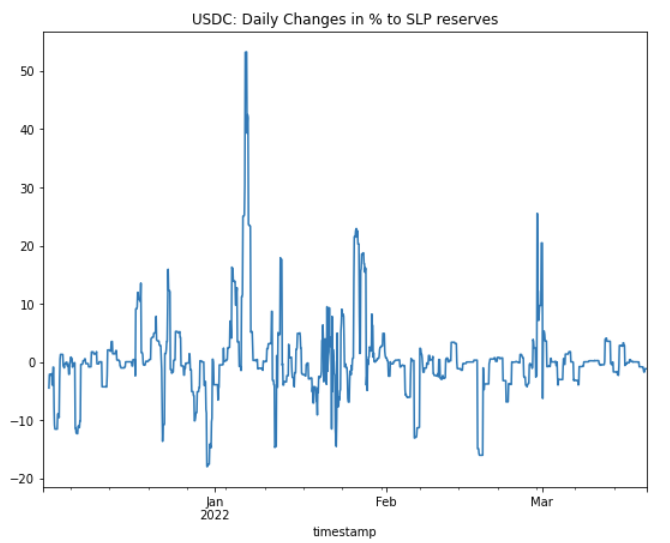

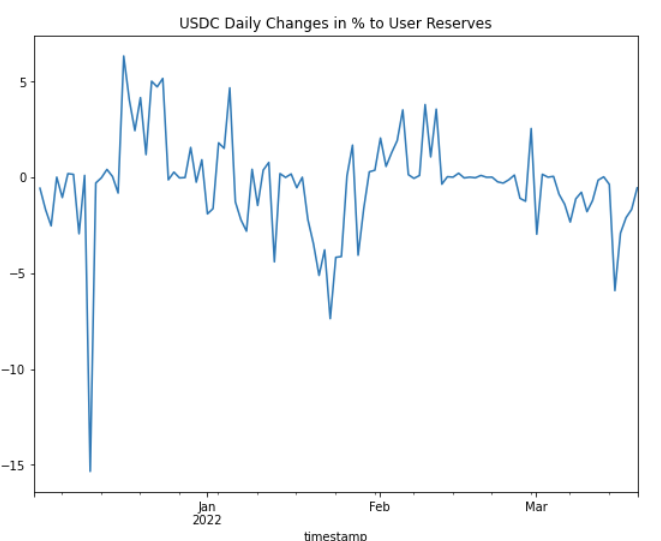

Below are the historical daily changes of user reserves and SLP reserves for DAI and USDC.

The DAI pool has had very stable user reserves since February with a couple of big withdrawals. The SLP reserves were more volatile but still very jumpy: approximately 3 times a month there has been a big redemption or deposit of c 10%. The USDC pool is more volatile but with similar jumps. It looks less concentrated than the DAI pool, probably because of its sizeBased on this historical data here is a summary of the parameters used:

Those parameters are then used to model probabilistically the daily changes in users and SLP reserves following the modeling framework described previously. We calculate the user reserves in EUR, the SLP reserves in USD, and then we FX it all to USD. We model the EUR/USD rate with a normal distribution and an annualized volatility of 5%.

Reserve analysis results

These results show the probability that the reserves in DAI and USDC will drop below certain levels over a three month and six month time horizon.

Calculating returns on early exit

The extra profit/loss realized versus lending on Compound will depend on:

- Remaining time to maturity. Notional trading fees are proportional to remaining maturity (30 bps p.a.). If you close a position with a 3 month remaining maturity, your total trading cost will be 7.5 bps (30 bps/4). The longer we wait before closing a position, the more extra fees we generate and the lower trading fees we will pay !

- Notional Interest Rate at which we close our position. This will determine our mark to market profit.

To make our calculation we use the following assumptions:

- In the event that Angle is forced to redeem some of its fixed rate loans, Angle will redeem 100% of its Notional positions.

- Early exit occurs halfway through the loan. For example, a 3 month loan will be exited after 1.5 months.

- The interest rate at exit equals the interest rate at inception.

This chart shows the excess return from lending on Notional vs Compound if Angle is forced to exit its loans early.

This table shows that Notional’s rates still provide excess returns even if Angle needs to exit its positions early.

Conclusion

Notional provides Angle an attractive place to put some of its capital and earn excess returns. The risks that fixed rate lending introduces are real, but this analysis shows that they are relatively small and easily managed. The excess returns that Notional offers makes fixed rate lending a worthwhile investment for Angle.

Notional Finance Newsletter

Join the newsletter to receive the latest updates in your inbox.