Fixed vs. Variable Rate Leverage - Which is Better?

Leveraged yield strategies are relatively new products in DeFi that allow users to potentially earn higher yields by taking on leverage that have proven to be popular with DeFi power users. Notional’s leveraged vaults, leveraged staking strategies on Aave, and money markets like Gearbox and Sentiment that are specifically designed to offer leveraged yield have all seen strong initial traction.

But with the exception of Notional’s leveraged vaults, all of these products use variable rate leverage instead of fixed rate leverage. With the launch of Notional V3, users will be able to choose between fixed and variable leverage for the first time and it’s not obvious which they should choose.

Each option has its pros and cons, but on balance we believe that fixed rates are a better fit for the leveraged yield strategy use case than variable rates for three reasons:

- The profitability of a leveraged yield strategy is highly sensitive to the borrowing rate - a small increase in that rate can tip the overall profitability of the strategy from highly positive to deeply negative.

- Variable borrow rates on money markets that offer leveraged yield strategies are highly volatile and prone to spikes. This causes degraded returns over time and occasional periods of massively negative overall APYs.

- Fixed rates allow the user to completely remove the risk of borrow rate volatility. This makes leveraged yield strategies built on fixed rates produce much more stable and reliable returns.

In this post, we will dig into the detail and examine historical borrow rate volatility on leveraged yield money markets and analyze simulated historical performance of an example leveraged yield strategy using fixed vs. variable rates. This analysis shows exactly how fixed rates reduce risk and what that means for users.

We will also discuss the downside of using fixed rate leverage - increased transaction cost. By making it more costly to enter and exit a leveraged yield strategy, fixed rates are less flexible than variable rates and require more of a commitment from the user. This makes fixed rate leverage more suitable for longer-term opportunities instead of highly short-term opportunities where variable rate leveraged may be better.

But first, what is a leveraged yield strategy?

Leveraged yield strategy explainer

A leveraged yield strategy uses borrowed funds to multiply a user’s exposure to a particular yield strategy and generate higher returns. Here’s an example of a leveraged yield strategy.

- Yield strategy: Deposit 100 ETH into the ETH/wstETH Balancer LP pool. Stake the Balancer LP tokens on Aura. Earn trading fees, ETH staking yield, and BAL + AURA incentives. Periodically harvest and reinvest the BAL and AURA incentives. Earn 5% Total APY.

- Leverage: Borrow 500 ETH from Notional at 4%. Invest the 500 borrowed ETH into the yield strategy in addition to the original 100 ETH. Now you have 600 ETH in the yield strategy earning 5% APY and 500 ETH debt costing 4% APY.

- Profit: You’re earning 5% APY on 600 ETH. Over a year that would be 30 ETH in total profit. You’re paying 4% APY on 500 ETH debt. Over a year that would be 20 ETH in total cost. That makes your total profit 10 ETH over the year (30 ETH gain - 20 ETH cost). 10 ETH profit on a 100 ETH deposit is 10% APY.

In this example, the user was able to use leverage to double the returns on their yield strategy from 5% APY to 10% APY. But leverage is not a free lunch. Using leverage can increase a user’s returns but it also introduces risks that can hurt the user’s returns or even cause them to lose money.

The risks of leveraged yield strategies

The main risk of a leveraged yield strategy is that the rate you’re paying to borrow is greater than the rate you’re earning on the yield strategy. To see this more clearly, here is the formula for calculating the total APY of a leveraged yield strategy:

Total APY = strategy APY + (strategy APY - borrow APY) * leverage

If the borrow APY is greater than the strategy APY, adding leverage decreases your overall returns. The more leverage you use, the worse it gets. Let’s compare the above example using a borrow rate of 4% vs. a borrow rate of 6%.

- 4% borrow rate: Total APY = 5% + (5% - 4%) * 5 = 5% + 5% = 10% APY

- 6% borrow rate: Total APY = 5% + (5% - 6%) * 5 = 5% - 5% = 0% APY

In the second case, the user isn’t making any return at all! Increasing the borrow rate by just 2% wiped out the user’s entire yield.

There’s two ways this can happen - the strategy yield goes down or the borrow rate goes up. Fixing your borrow rate allows you to completely remove the risk of the borrow rate increasing. And as we’ll see, a rising borrow rate is a much bigger risk for leveraged yield strategy users than a declining strategy yield.

Variable borrow rates in DeFi are highly volatile

Borrowing rates on money markets that allow users to get leverage on yield strategies are highly volatile and detrimental to leveraged yield strategy returns.

Some might point to major money markets like Compound and Aave and say that borrowing rates are actually very stable, and not volatile. This is true, but these money markets don’t allow users to get leverage on yield strategies so the borrow rates on these platforms are not relevant.

The borrow rates on money markets that do allow leveraged yield strategies are much more volatile because these platforms tend to be less liquid and have more borrowing demand. This results in borrowing rates that frequently spike higher past the kink on their interest rate curve which destroys returns for leveraged yield users.

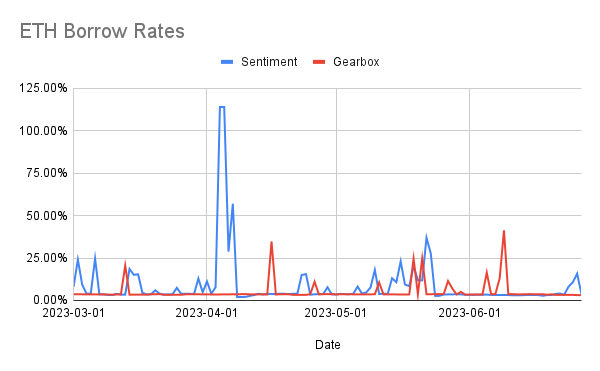

Here are ETH borrow rates since March 1st 2023 on two variable rate leveraged yield protocols, Gearbox and Sentiment.

ETH borrowing rates on these protocols were usually between 3% - 4% but they frequently spiked higher to 20%+ on Gearbox and even 100%+ on Sentiment. These frequent spikes meant that the average borrow rate for this period was 5.05% on Gearbox and 8.83% on Sentiment even though most of the time the rate stayed between 3% - 4%.

A high average borrowing rate means that even if your total APY looks good at entry, you will most likely end up earning less than you expected and you might even lose money. This will always be true for leveraged yield strategies based on variable rates because of two things:

- The borrowing rate has to spike during periods of high utilization. This is the only way that the money market can attract capital when it needs it and make the system safe for lenders.

- Leveraged yield strategy money markets frequently get into states of high utilization because they have lots of borrowing demand and relatively limited lending supply.

This means that the borrowing rate on leveraged yield strategies will regularly spike higher and reduce overall returns for leveraged yield strategies.

Fixed rates reduce risk

Fixing your borrowing rate allows you to remove your borrowing rate risk and more confidently make the decision to enter into a leveraged yield strategy. With a fixed borrowing rate, the only risk you have is that the strategy yield declines below your borrowing rate.

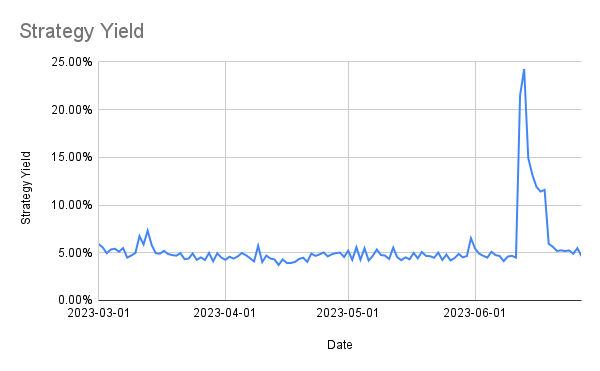

This is an easier risk to manage. Yield strategy returns are less volatile than variable borrowing rates. Additionally, when strategy yields spike it’s a GOOD thing for the user instead of a bad thing. For example, here are the returns to the wstETH/ETH strategy over the same period of time we looked at for the variable ETH borrowing rates on Gearbox and Sentiment.

The return on this strategy is relatively stable between 4% - 5%. And when the return changes significantly, the direction of the change is up! When you’re only exposed to variability in the yield strategy return, volatility spikes don’t hurt you, they help you.

This is because the downside on the strategy yield is limited in contrast to variable borrowing rates. The lowest the strategy yield can go is zero, and in practice LPs removing their liquidity gives the yield a higher floor than that. Variable borrow rates on the other hand can and do spike to over 20% frequently as we have seen.

Visualizing risk reduction with fixed rates

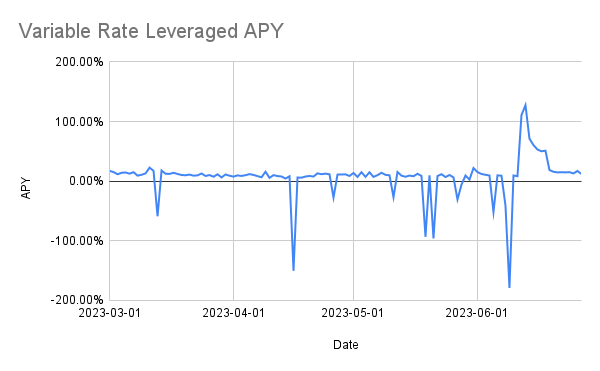

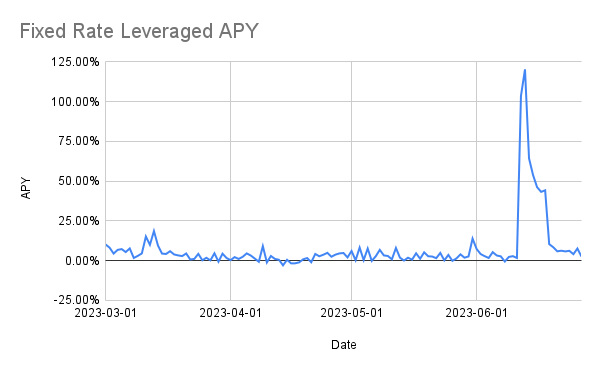

We can illustrate the impact that fixed rates have by using a historical comparison. Let’s examine the returns for two hypothetical users who entered into a 5x leveraged wstETH/ETH strategy - one that borrowed at the variable rate on Gearbox and one that borrowed at a fixed rate.

We will assume that the fixed rate was the average of the variable rate on Gearbox - this means that at the end of the period, each user would have made the same amount of money. But as we’ll see, the path to getting there would look very different for the two users.

Here are what their returns would have looked at using 5x leverage on the wstETH/ETH leverage strategy based on the variable borrow rate vs. a fixed rate of 5.05%.

If you were using variable rate leverage, you would have seen your total APY dip below -25% nine times over the time period and even get down to -179% APY at one point! With fixed rate leverage, your returns would have stayed relatively stable throughout the time period with the exception of a few times when the total APY spiked up, not down.

Even though the user would have made the same amount of money in either scenario, the volatility along the way is important because it can lead to bad decision-making. The urge to unwind your position when you’re looking at a -100% APY is strong. And if you do, you end up paying extra transaction fees and realizing a smaller return (or even a loss!) than if you had stayed comfy in a position with fixed rate leverage.

Transaction costs associated with entering and exiting a leveraged yield strategy are an important factor to consider, and this is one way that variable rate leverage has an edge over fixed rate leverage.

The downsides of fixed rate leverage - transaction costs

Entering and exiting a yield strategy involves two kinds of transaction cost - a strategy transaction cost and a borrow transaction cost. The strategy transaction cost occurs when you invest the assets into the strategy or redeem them from the strategy and is paid by all users, whether they borrow at a variable rate or a fixed rate.

The borrow transaction cost occurs when you take out or repay the loan, and this is where fixed rate leverage costs extra. The borrow transaction cost for variable rate leverage is zero. But for fixed rate leverage, this cost can be as large or larger than the strategy transaction cost depending on the maturity of the loan.

Transaction cost example

To see the effect of fixed rate leverage on overall transaction cost let’s look at the economics for two users who enter into the wstETH/ETH strategy with a 100 ETH deposit at 5x leverage using variable rate leverage vs. borrowing at a fixed rate for 3 months. We’ll assume that each user is earning a 10% total APY, and we’ll see their total transaction cost and calculate how long they will need to earn that 10% APY in order to break even.

Here’s how we calculate the strategy transaction cost:

- 600 ETH total deposited into the ETH/wstETH LP pool.

- LP pool is 50% ETH and 50% wstETH -> 300 ETH must be swapped for wstETH.

- ETH/wstETH swap fee is 0.04%

- Strategy transaction cost = 300 ETH * 0.04% = 0.12 ETH

Here’s how we calculate the fixed rate borrow cost:

- 500 ETH borrowed for 3 months.

- 0.3% borrow fee on the APY.

- Borrow fee = 0.3% / (3 months / 12 months in year) = 0.3% / 4 = 0.075%

- Borrow transaction cost = 500 ETH * 0.075% = 0.375 ETH

This gives the following total transaction costs for variable rate leverage vs. fixed rate leverage:

- Total transaction cost (variable leverage): 0.12 ETH

- Total transaction cost (fixed leverage): 0.495 ETH

In this case, the fixed rate borrow transaction cost is 3x+ the strategy transaction cost. That has a big impact on the users’ economics and how long it takes for them to break even:

- Days to break even (variable leverage): 4.38

- Days to break even (fixed leverage): 18.07

As you can see, using fixed rate leverage instead of variable rate leverage causes a big increase to a user’s total transaction cost and break-even point. This makes fixed rate leverage significantly less flexible than variable rate leverage.

The transaction cost in either case is non-trivial, so users probably won’t want to get in and out of a leveraged yield strategy that frequently anyway. But the increased transaction cost for fixed rate leverage means that this is even more true for users that borrow at a fixed rate.

Conclusion

Leveraged yield strategies are the new frontier for advanced DeFi users that want to increase the yield they earn on their assets. But these products are also risky and expose users to highly variable borrowing rates which can cause volatile yields and even losses.

Using fixed rate leverage instead of variable rate leverage can help users reduce their risk, stabilize their yield, and get a better understanding of their expected returns when they enter into a position.

But fixed rate leverage is not a free lunch - users need to be aware of the transaction cost associated with borrowing at a fixed rate and factor that into their decision making. Ultimately, if users expect to stay in a position for over a month, fixed rates are probably better whereas variable rates are more suited to short-term opportunities.

Notional Finance Newsletter

Join the newsletter to receive the latest updates in your inbox.