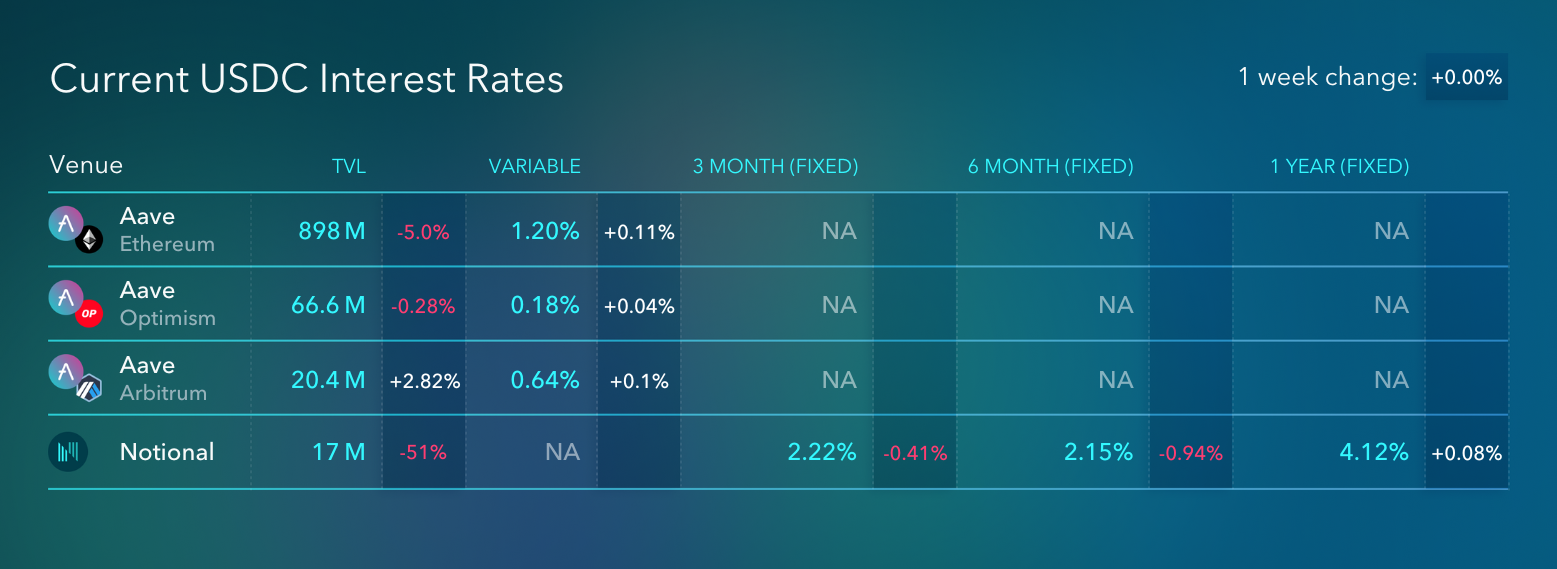

Weekly Interest Rate Roundup: Nov 29 - Dec 6

Contagion came for Maple Finance this week. $31M this time. On an absolute dollar basis it's not so bad relative to recent blowups, but this one hurt because it would appear to invalidate one of the last, if not THE last, remaining example of "CeFi lending done right". This failure begs the question, is such a thing even possible?

It started, as always, with some guy on twitter.

Maple UI is tricky, so fact check plz, but it appears Orthogonal is late on repayment in Maven 11 pool. A 60 day, 10 million USDC was drawn down 61 days and 17 hours ago... I don't see a corresponding repayment. @CharlieYouAI @TheDEFIac @EffortCapital https://t.co/mtkIQVu4iY https://t.co/XV21wGgnxM

— 0xSuperTrooper (@0xSuperTrooper) December 5, 2022

They were indeed late on repayment. The next morning, we got the official statement from the Maple credit delegate Maven 11:

On December 3rd, Orthogonal Trading informed us that due to funds held on FTX, they incurred a much larger loss than previously disclosed to us, and will not be able to repay loans or uphold their obligations as a borrower. https://t.co/VI6MfsNpOb

— M11 Credit (@M11Credit) December 5, 2022

1/3

From all public communications as well as from some conversations with people close to the situation, it appears that the losses imposed on Maple lenders in the Maven 11 USDC pool will be severe. On the order of ~80% of capital lent. Ouch.

Some say that this is simply part and parcel of uncollateralized lending. Lenders take the risk that something like this can happen and in return they are rewarded with high yields. Lenders should expect some amount of losses they say, and lenders were just particularly unlucky this time around.

But I think this misses the point. While yes, even the "best" lenders should expect some number of defaults, an outcome of this magnitude suggests that lenders were not getting nearly well enough compensated for the risk they were taking.

This is the central problem with CeFi lending platforms - the people putting in the money have no idea how much risk they are taking. Sure, maybe they know who they're lending to, but fat lot of good that does them apparently. And so the clearing price for the loans does not reflect their risk, it mostly just reflects the amount of deposits in the system.

This problem isn't new by the way. You can't expect retail depositors to go make loans and diligence prospective borrowers themselves. In Tradfi, this is solved by the federal backstop. If the bank goes belly-up, you still get your money back. In reality, the bank won't go belly-up because the government will bail them out. And because of this backstop, the government enforces all sorts of rules around capital requirements and things like that because it doesn't want to be left holding the bag for reckless lending practices.

But this isn't Tradfi. There is no federal backstop for crypto. What we have is the blockchain. The way we enforce capital requirements and lending practices is through smart contracts, not governmental regulations. Centralized actors that are free to operate without either smart contract enforced codes of behavior or regulatory requirements are not gonna make it. CeFi (or CeDeFi, or whatever) has proven to be the worst system of all. It's worse than DeFi, it's worse than Tradfi, and we can do better.

Teddy

Notional Finance Newsletter

Join the newsletter to receive the latest updates in your inbox.